Running a business, big or small, means dealing with numbers. But for many of us with not much accounting background, those accounting terms can feel like a foreign language. Here’s the thing, Go Remotely’s Accounting Statistics say that 60% of small business owners don’t feel knowledgeable about finances and accounting.

Don’t worry, you’re not alone. This guide breaks down 20 essential accounting terms every freelancer or small business owners needs to know. Let’s make sense of the numbers together.

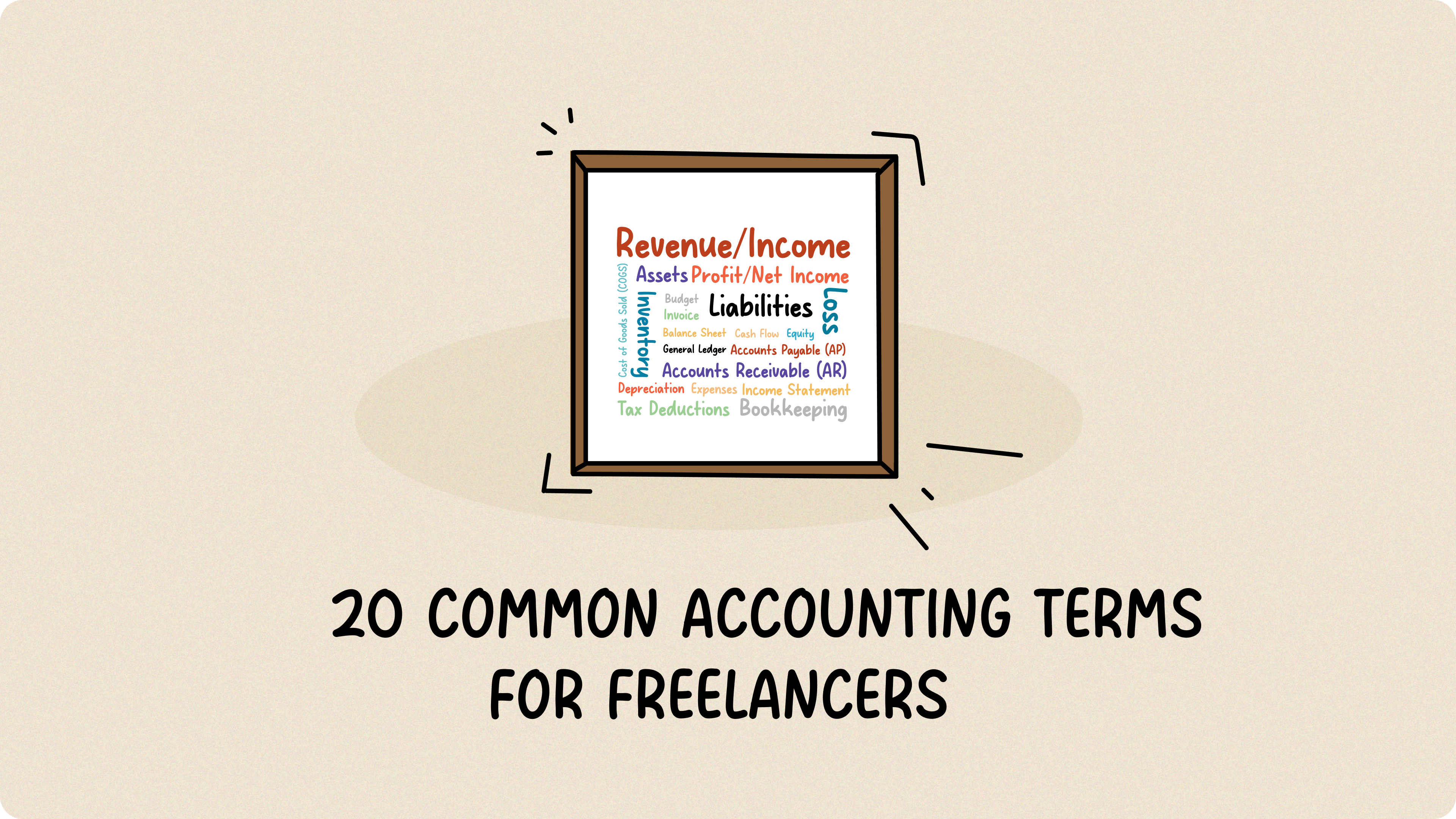

Your Financial Glossary

- Revenue/Income

- Expenses

- Profit/Net Income

- Loss

- Assets

- Liabilities

- Equity

- Cash Flow

- Accounts Payable (AP)

- Accounts Receivable (AR)

- Inventory

- Depreciation

- Cost of Goods Sold (COGS)

- Balance Sheet

- Income Statement

- General Ledger

- Tax Deductions

- Budget

- Invoice

- Bookkeeping

Let’s dive into each term, starting with:

1. Revenue/Income

Revenue is simply the total money your business brings in from sales or services. Think of it as your gross income, before you subtract any expenses.

2. Expenses

Expenses are what you spend to keep your business running and generate revenue. Here are the main types:

- Fixed expenses: These are your regular, predictable costs that stay pretty consistent month to month, regardless of how busy or slow your business is, like rent, wages, loan payments, and insurance premiums.

- Variable expenses: These change depending on how much you sell or produce. Consider food ingredients for restaurants, shipping for online stores, or utilities that fluctuate with usage.

- Accrued expenses: These are expenses you’ve incurred but haven’t paid yet, such as taxes owed or accrued interest on loans.

- Operational expenses: These are your day-to-day costs, excluding the direct cost of producing goods or services, like marketing, advertising, and office supplies.

3. Profit/Net Income

Profit is essentially the financial gain your business achieves when your revenue, the money you bring in, surpasses your expenses, the money you spend. To put it simply, it’s what you get to keep. So, for example, if your business generated $10,000 in revenue and you incurred $6,000 in expenses, you’d end up with a profit of $4,000.

4. Loss

A loss is the opposite: when your expenses are higher than your revenue. If you spent $8,000 and only made $5,000, you’ve got a $3,000 loss. This trend is not sustainable in the long term.

5. Assets

Assets are anything your business owns that has value, from cash and equipment to your laptop or even your website and intellectual property.

6. Liabilities

Liabilities are what your business owes to others, like loans, supplier payments, and credit card balances.

7. Equity

Equity is essentially your net worth in the business. It’s what would be left if you sold all your assets and paid off all your debts.

8. Cash Flow

Cash flow is the movement of money in and out of your business over a period of time. It’s about having enough cash on hand to pay the bills. Even profitable businesses can struggle with poor cash flow. (Check out our blog on Cash Flow Projection!)

9. Accounts Payable (AP)

Accounts Payable (AP) represents the money your business owes to suppliers or other creditors for goods or services received but not yet paid. For instance, if you’ve received inventory or supplies on credit and haven’t paid the invoice yet, that amount is considered Accounts Payable.

10. Accounts Receivable (AR)

Accounts Receivable (AR), on the other hand, is the money your customers owe your business for goods or services you’ve already delivered or provided. It’s the opposite of Accounts Payable; it’s money coming in. For example, if you’ve sent an invoice for $500 for services rendered and the customer hasn’t paid yet, that $500 is an Accounts Receivable. It’s important to track AR carefully, as it directly impacts your cash flow and ability to cover your own expenses.

11. Inventory

Inventory refers to the goods your business holds for sale. It’s the items you have on hand, ready to meet customer demand. In essence, effective inventory management is crucial. You don’t want to run out of stock and lose sales, but you also don’t want too much stock sitting around, which leads to waste and ties up your capital.

12. Depreciation

Depreciation is the gradual loss of value of your assets over time, like a restaurant oven getting older. It’s recorded as an expense on your income statement.

13. Cost of Goods Sold (COGS)

COGS is the direct cost of producing your goods, including materials and labor. For a restaurant, it’s the cost of ingredients and food preparation. For an online shop selling handmade crafts, it’s the cost of raw materials like fabric and yarn, plus the labor involved in creating the finished products.

14. Balance Sheet

A balance sheet is a financial picture of your business at a specific moment, showing what your business owns (your assets), who your business owes money to (your liabilities), and how much you, the owner, have invested (your equity). It’s based on the equation: Assets = Liabilities + Equity. (Learn more about balance sheets here.)

15. Income Statement

An income statement shows your business’s revenue, expenses, and profit or loss over a specific period (e.g., a month or a year). It tells you how well your business performed during that time.

So, how does it differ from a balance sheet? Well, a balance sheet provides a snapshot of your business’s financial position at a specific moment, while the income statement focuses on your performance over time. They work together to give you a full picture of your financial health.

16. General Ledger

The general ledger is the comprehensive record that organizes all your business’s financial transactions. Imagine it as a detailed logbook of every financial event, categorized by type, such as sales, expenses, and asset changes. This organization makes it easy to see the complete picture of your business’s financial activity and is the backbone of your accounting system.

17. Tax Deductions

Tax deductions are expenses you can subtract from your income to lower your tax bill. (Want some crazy tax deduction examples? Check out these approved deductions!)

18. Budget

A budget is your financial plan for a future period, showing your estimated revenue and expenses. It’s usually re-evaluated regularly to ensure it remains accurate and reflects the current state of your business.

19. Invoice

An invoice is a bill you send to your customers for goods or services you’ve provided. It details what they owe you and when it’s due.

20. Bookkeeping

Bookkeeping is the essential process of recording and organizing your business’s financial transactions. It’s about keeping a detailed record of every dollar that comes in and goes out, like customer payments and vendor bills. While it used to be done in physical ledgers, modern bookkeeping is largely handled by digital software, making it more efficient and accurate.

So, there you have it, 20 accounting terms you need to know as a business owner or freelancer.

With Fynlo, knowing these terms is enough to get you through tax season. We can handle all the complex bookkeeping, so you can focus on growing your business without worrying about the jargon. Schedule a call with us!