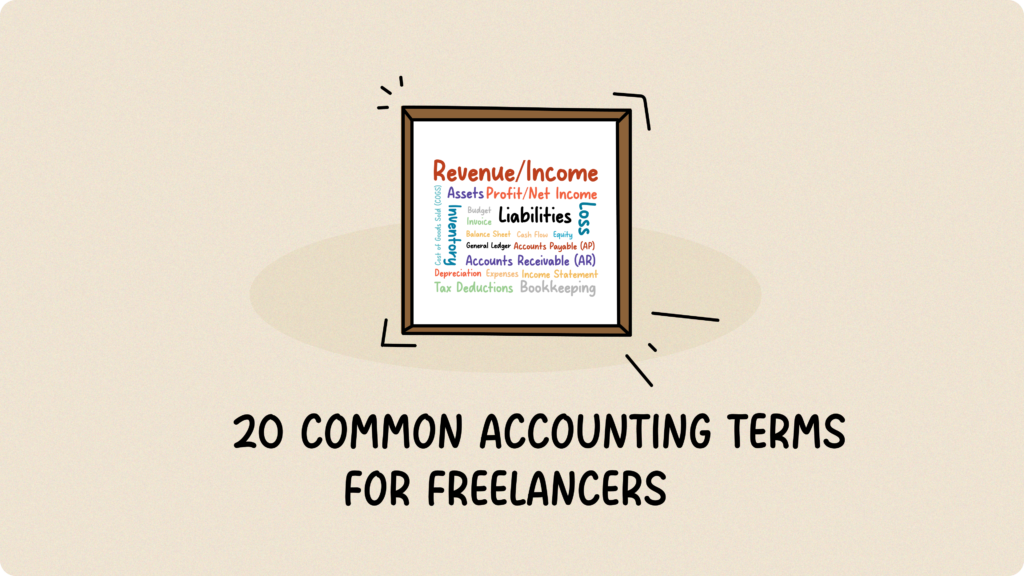

20 Common Accounting Terms for Freelancers

Running a business, big or small, means dealing with numbers. But for many of us with not much accounting background, those accounting terms can feel like a foreign language. Here’s the thing, Go Remotely’s Accounting Statistics say that 60% of small business owners don’t feel knowledgeable about finances and accounting. Don’t worry, you’re not alone. This guide breaks down 20 essential accounting terms every freelancer or small business owners needs to know. Let’s make sense of the numbers together. Your Financial Glossary Let’s dive into each term, starting with: 1. Revenue/Income Revenue is simply the total money your business brings in from sales or services. Think of it as your gross income, before you subtract any expenses. 2. Expenses Expenses are what you spend to keep your business running and generate revenue. Here are the main types: 3. Profit/Net Income Profit is essentially the financial gain your business achieves when your revenue, the money you bring in, surpasses your expenses, the money you spend. To put it simply, it’s what you get to keep. So, for example, if your business generated $10,000 in revenue and you incurred $6,000 in expenses, you’d end up with a profit of $4,000. 4. Loss A loss is the opposite: when your expenses are higher than your revenue. If you spent $8,000 and only made $5,000, you’ve got a $3,000 loss. This trend is not sustainable in the long term. 5. Assets Assets are anything your business owns that has value, from cash and equipment to your laptop or even your website and intellectual property. 6. Liabilities Liabilities are what your business owes to others, like loans, supplier payments, and credit card balances. 7. Equity Equity is essentially your net worth in the business. It’s what would be left if you sold all your assets and paid off all your debts. 8. Cash Flow Cash flow is the movement of money in and out of your business over a period of time. It’s about having enough cash on hand to pay the bills. Even profitable businesses can struggle with poor cash flow. (Check out our blog on Cash Flow Projection!) 9. Accounts Payable (AP) Accounts Payable (AP) represents the money your business owes to suppliers or other creditors for goods or services received but not yet paid. For instance, if you’ve received inventory or supplies on credit and haven’t paid the invoice yet, that amount is considered Accounts Payable. 10. Accounts Receivable (AR) Accounts Receivable (AR), on the other hand, is the money your customers owe your business for goods or services you’ve already delivered or provided. It’s the opposite of Accounts Payable; it’s money coming in. For example, if you’ve sent an invoice for $500 for services rendered and the customer hasn’t paid yet, that $500 is an Accounts Receivable. It’s important to track AR carefully, as it directly impacts your cash flow and ability to cover your own expenses. 11. Inventory Inventory refers to the goods your business holds for sale. It’s the items you have on hand, ready to meet customer demand. In essence, effective inventory management is crucial. You don’t want to run out of stock and lose sales, but you also don’t want too much stock sitting around, which leads to waste and ties up your capital. 12. Depreciation Depreciation is the gradual loss of value of your assets over time, like a restaurant oven getting older. It’s recorded as an expense on your income statement. 13. Cost of Goods Sold (COGS) COGS is the direct cost of producing your goods, including materials and labor. For a restaurant, it’s the cost of ingredients and food preparation. For an online shop selling handmade crafts, it’s the cost of raw materials like fabric and yarn, plus the labor involved in creating the finished products. 14. Balance Sheet A balance sheet is a financial picture of your business at a specific moment, showing what your business owns (your assets), who your business owes money to (your liabilities), and how much you, the owner, have invested (your equity). It’s based on the equation: Assets = Liabilities + Equity. (Learn more about balance sheets here.) 15. Income Statement An income statement shows your business’s revenue, expenses, and profit or loss over a specific period (e.g., a month or a year). It tells you how well your business performed during that time. So, how does it differ from a balance sheet? Well, a balance sheet provides a snapshot of your business’s financial position at a specific moment, while the income statement focuses on your performance over time. They work together to give you a full picture of your financial health. 16. General Ledger The general ledger is the comprehensive record that organizes all your business’s financial transactions. Imagine it as a detailed logbook of every financial event, categorized by type, such as sales, expenses, and asset changes. This organization makes it easy to see the complete picture of your business’s financial activity and is the backbone of your accounting system. 17. Tax Deductions Tax deductions are expenses you can subtract from your income to lower your tax bill. (Want some crazy tax deduction examples? Check out these approved deductions!) 18. Budget A budget is your financial plan for a future period, showing your estimated revenue and expenses. It’s usually re-evaluated regularly to ensure it remains accurate and reflects the current state of your business. 19. Invoice An invoice is a bill you send to your customers for goods or services you’ve provided. It details what they owe you and when it’s due. 20. Bookkeeping Bookkeeping is the essential process of recording and organizing your business’s financial transactions. It’s about keeping a detailed record of every dollar that comes in and goes out, like customer payments and vendor bills. While it used to be done in physical ledgers, modern bookkeeping is largely handled by digital software, making it more efficient and accurate. So, there you have it, 20 accounting terms you need to know as

Restaurant Owners: A Beginner’s Guide to Creating a Business Plan

You’ve got the vision—your very own restaurant! Whether it’s a cozy café, a bustling bistro, or a lively food truck, before you fire up the grill or brew that first pot of coffee, you’ll need a solid business plan. Think of it as your key to success. By working through the hard parts, you’ll gain a clear and focused understanding of what it takes to succeed. With all the right pieces in place, it’s a document you can complete in a day. This guide walks you through the essential steps to create one and includes links to a free, easy-to-use template to help you get started today. Table of Contents What is Business Planning? Before you even think about opening your restaurant, you’ve probably got a million questions swirling in your head: What kind of food are we serving? Who’s our ideal customer? How much is this whole thing going to cost, and when do we start seeing a profit? How are we going to get the word out? You’re basically trying to piece together a puzzle, and that’s exactly what a business plan does: it gathers all those puzzle pieces into one clear picture. Think of it like a roadmap for your restaurant’s journey. It takes all those initial ideas and turns them into a structured plan, outlining the route you’re going to take. With this map in hand, you’re not just keeping yourself on track, you’re creating a reference point for everyone involved. The business plan is also important to our stakeholders, for example investors can access the financial projections, potential partners would understand the direction and consider if they would collaborate. It’s all about showing people the whole plan clearly and align everyone’s expectation. What are the Essential Parts of a Business Plan? Section 1: Executive SummaryAn executive summary is like a strategic brief. It’s a short, compelling preview that captures the essence of your business plan, enticing potential investors and partners to want to know more. It’s a narrative designed to spark interest by highlighting the most compelling aspects. Here’s what you’ll want to include: Section 2: Unique Selling Proposition (USP)This section details your restaurant’s Unique Selling Proposition (USP), articulating what distinguishes it from competitors and why it is poised for success. It addresses fundamental questions: What specific problem does your restaurant solve for its target market? How does it effectively provide the solution? For instance, you might identify an underserved niche, such as the lack of authentic Turkish cuisine in a thriving business district, or capitalize on a recent market shift, like the closure of a popular restaurant creating a demand gap. Therefore, this summary should describe your industry, your restaurant’s location, and its distinguishing features. Will you specialize in gourmet burgers near a sports arena? Feature a family recipe that’s a local sensation? Clearly convey your vision for success to your readers. Section 3: Competitive AnalysisBefore launching your restaurant, understanding the local food scene isn’t just helpful, it’s essential for long-term success. In this part of your business plan, you’ll explain how your restaurant will navigate the competitive landscape. And remember, your competition isn’t limited to just similar restaurants, it also includes meal delivery services, grocery stores with ready-to-eat options, and even entertainment venues that serve food and drinks. Doing your homework like visiting other spots to check out customer demographics, menu styles, pricing, and overall vibe, can give you valuable insights into what’s working (and what’s not) in your area. The goal here is to reduce risk and uncover real opportunities. A solid competitive analysis helps you spot gaps in the market, understand what your potential customers are looking for, and learn from what others are doing—both the good and the not-so-good. Section 4: Food OfferingsNow that you know well about your competitors, it’s time to think of what you’ll sell and how they are priced. Generally, the pricing should balance ingredient costs and what your target customers are willing to pay based on local market conditions. Design your menu for operational efficiency. Utilizing overlapping ingredients across multiple dishes can minimize food waste and reduce overall operational expenses. Consider highlighting high-margin items, such as coffee, beverages, and desserts, depending on your restaurant’s concept. Implement bundled deals to encourage higher per-customer spending. Think of a signature item for your restaurant, like the glazed doughnuts at Krispy Kreme or the fried chicken at KFC. People visit specifically for that standout dish, and often end up buying other items too. Section 5: MarketingWhat are your strategies for getting the word out about your restaurant? Will you advertise with KOLs, run ads on social media, distribute leaflets to nearby residents or offices, or offer special promotions for students? Try to estimate the cost of each marketing channel and the number of customers it may attract. In other words, calculate the customer acquisition cost. Explain why you believe the channels you’ve chosen are the most effective for reaching your target audience. And don’t forget, you’ll want to build a strong brand identity too, something that’ll keep people coming back for more. Once you have written this section, take a step back and read it from an investor’s perspective. Does it inspire confidence? Does it make you want to invest? If the answer is yes, great job. This section is doing its job well. Section 6: Operation PlanThis section explains how you’ll run your restaurant on a day-to-day basis, from setting up the space to managing everyday operations. You’ll want to think through all the important details, including your restaurant layout, how many staff you’ll need, what equipment to purchase, where to source your supplies, and the key costs involved, such as rent, wages, ingredients, and technology. Using the right tools will make life a lot easier. For example, a POS system can help your customers pay quickly and accurately. You might use an inventory system to keep track of stock, a clock-in tool to manage staff hours, and accounting software to stay on top of

10 Signs of a Bad Bookkeeper to Absolutely Avoid

Whether you’re a startup or a growing small business, knowing your financial status is key to keeping your business on track. Whether you work with bookkeeping software that offers support, a part-time bookkeeper, or external accountants, it’s crucial to ensure they are doing their job properly, making your life easier, not harder. Good bookkeepers are your financial peace of mind, keeping things organized and making sure you are compliant. But bad ones can drain your profits and intensify your tax nightmares. Is your bookkeeper the right fit? Read on for 10 troubling signs that it may be time to find a new bookkeeping solution. 10 signs of a Bad Bookkeeper Why Fynlo is a Trusted Solution If you’ve recognized one (or more) of the signs of a bad bookkeeper in your current service, it’s time to consider a reliable alternative. At Fynlo, we understand the challenges of financial management firsthand. That’s why we’ve built an intuitive platform designed to simplify your financial life and put you back in control. Fynlo provides access to seasoned accounting professionals. Our junior accountants bring over five years of experience, while our senior accountants boast more than ten years, most honed at top-tier firms like the Big Four, Baker Tilly, BDO, and Grant Thornton. We also prioritize confidentiality and data security. Every client relationship includes a signed Non-Disclosure Agreement (NDA), so your sensitive financial data is protected at all times. Here’s how Fynlo can benefit your business: Click here to schedule a call with our expert and take the stress out of bookkeeping. Fynlo team can handle everything from categorizing your transactions and reconciling your accounts to delivering precise, tax-ready financial statements.

10 Metrics Restaurant Owners Should Track to Boost Profits and Efficiency

Running a restaurant is no small feat. From managing substantial investments and fluctuating food prices to handling high employee turnover and ensuring regulatory compliance, the challenges are numerous. Not to mention the constant concerns about utility bills and food waste. A recent study indicates that while average restaurant revenues can range from 0% to 15%, profit margins typically hover between 3% and 5%. Daniel of POV Husband recently shared the monthly performance of three restaurants. He noted each restaurant is unique, with numbers varying monthly. During a snapshot month, his restaurants achieved the following: Restaurant Gross Sales Gross Profit Net Income Profit Margin A $119,861 $76,902 $20,463 15% B $70,927 $45,582 $9,001 13% C $256,108 $171,156 $59,783 23% Notice the trend: as restaurants scale, efficiency and profit margins tend to increase, highlighting the challenge for startups. Small restaurants, with minimal room for error, must leverage metrics for data-driven decisions. By using metrics, they can implement effective solutions—like optimizing ingredient costs or refining staffing schedules—instead of resorting to knee-jerk reactions like raising prices. In this article, we’ll explore 10 essential metrics that empower smaller restaurants to thrive. Table of Contents Why Metrics Matter Just as a great dish relies on the right ingredients, a successful restaurant depends on tracking the right metrics. Restaurant owners excel at crafting recipes and selecting high-quality ingredients, but many overlook the “ingredients of success”—the key performance indicators that fuel profitability and efficiency. A metric is any quantifiable, consistently defined measurement of performance. Two decades ago, data and metrics might not have been a focal point in the restaurant industry. However, in today’s competitive landscape, metrics offer invaluable insights into your restaurant’s effectiveness. They help identify strengths and pinpoint areas needing improvement, allowing for informed adjustments to operations and strategies aimed at optimizing profits. Often referred to as Key Performance Indicators (KPIs), these metrics provide a detailed picture of your overall business performance and indicate whether you’re on track to meet your goals. On top of that, understanding your customers through data enables targeted marketing efforts, enhancing sales strategically. For instance, if you know a customer dines out every Friday, you can send them a timely email on Friday afternoon. If you’re aware of an upcoming birthday, offering a complimentary champagne can enhance their experience. Recognizing big spenders allows for tailored loyalty rewards. Understanding spending habits, such as increased spending at month’s end, enables precise targeting. Knowing a customer’s preference for brownies allows for personalized suggestions during ordering. Restaurants that collect and effectively utilize data are poised for success. The pertinent question then becomes: which metrics should we track? 10 Metrics to Help Your Restaurant Thrive 1. Table Turnover Rate This metric tracks how efficiently you’re using your seating capacity. It measures how many times a table is “turned over” or reset for a new party during a specific meal service, like lunch or dinner. More turns generally mean more customers served and increased revenue, but it’s crucial to find a balance that doesn’t compromise the guest experience. You don’t want to rush diners out the door, but you also don’t want tables sitting empty for extended periods. To calculate the table turnover rate, you use the following formula: Table Turnover Rate = Parties Served ÷ Number of Tables For example, if a restaurant with 50 tables serves 200 customer parties during dinner service, the table turnover rate would be 4. This means each table was used an average of 4 times during that period. The industry benchmark for table turnover rate is around 3. This means that, on average, a table in a typical restaurant is used three times during a given meal service, like lunch or dinner. However, this is just a general guideline. Your ideal table turnover rate will depend on factors like: Target audience: A business lunch crowd might expect faster service than a leisurely dinner crowd. Table size and configuration: Smaller tables generally turn over faster than larger ones. To optimize your table turnover rate, focus on creating efficient systems and processes. This includes providing prompt and attentive service, from order taking to food delivery and table clearing. A well-designed restaurant layout can also contribute to smoother flow and faster turnover. 2. Average Check Size Average check size, also known as average customer spend, is a key metric that reveals the average amount each customer spends per visit. This valuable insight helps you understand customer behavior, assess the effectiveness of your menu pricing, and identify opportunities to increase revenue. By analyzing and optimizing the average check size, you can strategically implement upselling or cross-selling techniques to drive more revenue per customer. Here’s how to calculate the average check size: Average Customer Spend = Total Revenue ÷ Number of Customers For example, if your restaurant generated $5,000 in revenue from 200 customers in a day, your average check size would be $25 ($5000 ÷ 200 = $25). Industry benchmarks for average check size vary depending on the type of restaurant. Coffee shops typically have an average check of around $11, while quick-service restaurants range from $8 to $15. Casual dining establishments average between $12 and $15, while upscale full-service restaurants can range from $16 to $25. Fine dining establishments, of course, have significantly higher average checks, often ranging from $50 to $500 or more. There are several strategies you can implement to increase your average check size. These include providing excellent customer service, ensuring your staff has thorough menu knowledge, offering enticing specials, and using high-quality ingredients that justify higher prices. 3. Food Cost Percentage Food cost percentage is a critical metric that reveals how much of your revenue is spent on food and beverages. Given that 52% of restaurant professionals identify high food costs as a top challenge (according to Toast’s Restaurant Success Report), keeping this percentage in check is essential for profitability. By monitoring your food cost percentage, you can make informed decisions about menu pricing and cost control, ultimately protecting your restaurant’s financial health. Food cost percentage is calculated as follows: Food Cost Percentage = Total Food

How Ryan Robinson & Justin Welsh Scaled Freelancing into a Six-Figure Business

Let’s face it: as a freelance content marketer, you’re up against stiff competition. The field is overflowing with talented individuals vying for the same opportunities. But don’t let that discourage you! Countless freelance content marketers are not just surviving, but thriving in this competitive landscape. Want to know how they did it? In this article, we’ll dive deep into the journeys of five successful freelance content marketers, uncovering the strategies and mindsets that propelled them to the top. Get ready to be inspired and learn how you can apply their lessons to your own freelance career. Table of Contents Ryan Robinson: From Failure to a $35K/Month Blog Empire Ryan Robinson wasn’t an overnight success—he built his empire from scratch. After multiple entrepreneurial failures, he took a different approach: documenting his journey. What started as a side project—RyRob.com—soon became a go-to resource for freelancers and entrepreneurs looking to grow online. With 500,000+ monthly readers and 250,000 email subscribers, Ryan has mastered the art of SEO, affiliate marketing, and content monetization. His blog now generates $25,000 to $35,000 per month, proving that strategic content creation is a powerful business model. But he didn’t stop there—he co-founded RightBlogger, a suite of 80+ tools for bloggers, filling the gap he wished existed when he started. Beyond his blog, Ryan has worked with LinkedIn, Zendesk, Adobe, Google, and other Fortune 500 brands, helping them grow through high-impact content marketing. His expertise has been featured in Forbes, Fast Company, Business Insider, and Entrepreneur. Here are some of his most impactful insights: “It takes time to make money blogging. In fact, it takes a good deal of time to make money blogging.” “You’ll Make Mistakes with a New Blog and That’s Okay (in Fact, it’s Vital)” “Quality is Much More Important than Quantity with a New Blog.” Justin Welsh: From Corporate Burnout to Million-Dollar Solopreneur Justin Welsh wasn’t just another corporate executive—he was a high-performing leader in the SaaS world. Over the last decade, he played a pivotal role in scaling two companies past a $1 billion valuation and helped raise over $300 million in venture capital. His expertise in growth, sales, and strategy made him a powerhouse in the startup ecosystem. But despite his impressive achievements, something was missing. By 2019, burnout had taken its toll. The relentless grind, high-pressure environment, and constant chase for the next milestone left him drained. He realized that while he was helping companies succeed, he wasn’t designing a life that fulfilled him. So, he made a bold move—he and his wife quit their high-paying jobs, packed up their lives, and moved to the Catskill Mountains in New York to start fresh. Rather than jumping into another corporate role, Justin decided to build something of his own. He turned his knowledge of business, marketing, and personal branding into a thriving one-person business. Starting with LinkedIn, he crafted a strategy of sharing actionable insights, industry wisdom, and personal reflections—consistently and authentically. Over time, he grew his audience to over 700,000 followers and became one of the most influential solopreneurs on the platform. But he didn’t stop at content creation. Justin monetized his expertise through digital products and coaching, focusing on simplicity and scalable systems. His courses, including The LinkedIn Operating System, have helped thousands of professionals build their brands and businesses. His model? One niche. One clear problem. One systematized solution. No unnecessary complexity. Justin’s Key Lessons for Solopreneur Success: “You should have a very “long game’ mentality.“ Start a side project. Build it to 60% of your salary. Then go all in.” “The solopreneur playbook is simple: One niche. 1,000 true fans. One solvable problem. One systematized solution. Everything else is just overcomplication.” “The most successful people I know don’t have better ideas. They have a higher tolerance for discomfort. They’re simply willing to sit in the mess longer than everyone else.” Miranda Marquit: From $5 Articles to Six-Figure Financial Writer Miranda Marquit’s journey as a freelance writer didn’t start with six-figure clients or prestigious bylines—it began with $5 keyword-stuffed articles for content mills. Like many freelancers, she started at the bottom, taking low-paying gigs just to gain experience. But she knew she couldn’t stay there. Instead of grinding away for pennies, she made a strategic decision to specialize in a lucrative niche: personal finance. At first, Miranda wrote for independent bloggers, gradually building her portfolio and credibility. As her expertise grew, she transitioned into corporate clients—banks, fintech firms, and investment companies that valued her deep knowledge of finance. With each step, she increased her rates, moving away from the content mills and into the world of high-paying clients. But it wasn’t just her financial expertise that set her apart—it was her commitment to quality, networking, and long-term relationships. Miranda actively engaged in finance writing communities, built strong professional connections, and positioned herself as a thought leader in her niche. Over time, she secured premium clients, established herself as a go-to financial writer, and turned her freelance work into a sustainable six-figure career. Miranda’s Takeaways for Aspiring Freelance Writers: “There are so many great opportunities, and I’d hate for people to be afraid to try just because they feel they don’t have the time.” “My favorite moments are when readers email to let me know that something I wrote taught them something new or encouraged them to think about money in a different way.” “Try to make those personal connections and, most of all, try to be useful. That personal connection really does make a difference.” Bani Kaur: The Fearless Freelancer Who Faked It Until She Made It “Can you write for our SaaS?” The voice on the other end asked. Without hesitation, Bani Kaur replied, “Yes, of course.” The truth was, she had never written about SaaS before. Up until that moment, her writing experience was rooted in architectural publications. But instead of letting inexperience hold her back, she hung up the phone and immediately Googled, “What is SaaS?”—and so began her crash course into the tech industry.

Tax Filing Guide for S Corp, C Corp and LLC

Picking the right business structure is a big deal, and taxes are a huge part of that decision. In this article, we’re breaking down the tax filing side of things for C Corps, S Corps, and LLCs, so freelancers and business owners can get a handle on the forms and deadlines for each. If you’re looking for a broader comparison, Choosing the Best Business Structure for Freelancers is a solid starting point! The article was last updated as of 4 March 2025. Keep in mind that tax rules and limits can change, so be sure to watch out for updates or consult a tax professional for the latest information. Table of Contents Brief Highlights: Comparing C Corp, S Corp and LLC Here’s a quick rundown of the three business structures to give you the big picture. In the next sections, we’ll break down the details of tax treatment and the specific forms you’ll need to know. It’ll all come together as we go. Category S Corporation (S Corp) C Corporation (C Corp) Limited Liability Company (LLC) Tax Forms – Form 1120-S– Shareholders file Schedule K-1 on personal returns – Form 1120 – Shareholders report dividends on personal returns Depends on tax classification. See LLC section. Filing Deadlines March 15 2025*; extensions available April 15 2025*; extensions available Depends on tax classification. See LLC section. State Taxes Varies; some states do not recognize S Corp status Subject to state corporate income taxes Subject to state taxes depending on classification Eligibility Requirements – Must be a domestic business– Up to 100 shareholders – Individuals only – No limit on shareholders– Can include foreign and corporate owners – No ownership restrictions – Flexible member structure Ownership Restrictions – Max 100 shareholders– One class of stock– U.S. citizens/residents only – Unlimited shareholders– Can issue multiple stock classes – No restrictions– Members can be individuals, corporations, or foreign entities Compliance Requirements – Annual meetings– Shareholder voting– File annual reports – Annual meetings– Corporate governance– Strict record-keeping – Varies by state– Fewer formalities than corporations Average Formation Costs# ~$1,200 ~$633 ~$50-$500 depending on state Fundraising Ability – Limited– Cannot issue preferred stock – High– Can issue both common and preferred stock Limited unless electing C Corp tax treatment Dividend Taxation Distributions taxed once at shareholder level Dividends taxed twice (corporate and shareholder level) Not applicable unless taxed as C Corp Payroll Tax Implications Must pay reasonable salary to shareholder-employees Corporate officers are employees subject to payroll taxes Members typically pay self-employment tax unless S Corp election made Passive Income Limits (such as rent, interest, or certain royalties) Passive income limited to 25% of gross receipts No passive income limitations No passive income restrictions Liability Protection Protects shareholders’ personal assets Protects shareholders’ personal assets Protects members’ personal assets Conversion Flexibility Can convert to C Corp; changing to LLC requires dissolution Can convert to S Corp or LLC with filings and approvals Can elect S Corp/C Corp taxation; conversions depend on state rules Foreign Ownership Not allowed Allowed Allowed Administrative Burden Higher than LLC; less than C Corp High due to strict governance requirements Low; fewer formalities required Key Tax Advantages – Avoids double taxation– QBI deduction available – Potential for certain deductions not available to pass-through entities– Can deduct health insurance premiums for employees – Flexible tax treatment (can choose to be taxed as a partnership, S corp, or C corp)– Simpler tax compliance than C-corp if taxed as a partnership Key Tax Disadvantages – Reasonable salary requirement– Limitations on QBI deduction for certain businesses – Double taxation– More complex tax compliance – Members subject to self-employment tax (unless taxed as C-corp)– Less established than C-corps in some states Best For Small businesses seeking tax savings through pass-through taxation Larger businesses seeking growth through investment and stock issuance Startups, freelancers, or small businesses needing flexibility * For calendar-year corporations, Form 1120 is due on April 15, and Form 1120-S is due on March 15. For fiscal-year corporations, the deadline is the 15th day of the fourth month (1120) or third month (1120-S) after the fiscal year ends. # Formation costs vary by state and the scope of professional services. S Corporations Tax Filing S corps offer a unique tax structure, blending the legal benefits of a corporation with the tax advantages of a partnership. This pass-through taxation model avoids the double taxation burden of C corporations, making it an attractive option for many small businesses. Pass-Through Taxation One of the most significant advantages of an S corporation is its pass-through taxation model. Unlike C corporations, which are subject to double taxation (taxed at both the corporate and shareholder levels), S corps do not pay federal income tax at the corporate level. Instead, the corporation’s profits and losses are passed through to the shareholders, who report them on their individual tax returns (Form 1040). This structure avoids the double taxation burden and can result in significant tax savings for business owners. Form 1120-S Form 1120-S, the U.S. Income Tax Return for an S Corporation, is the primary form S corps use to report income, deductions, gains, and losses to the IRS. It ensures the corporation’s financial activity is accurately reported and provides shareholders with the information needed to complete their individual tax returns. The form is due by March 15th for calendar-year taxpayers (or the 15th day of the third month after the fiscal year ends). If additional time is needed to prepare the return, S corps can request an extension using Form 7004, which grants an automatic six-month extension. However, it’s important to note that an extension to file does not extend the deadline for paying any taxes owed. Estimated tax payments must still be made by the original due date to avoid penalties and interest. Schedule K-1 Schedule K-1 details each shareholder’s individual share of the corporation’s income, deductions, credits, and other tax items. Shareholders use this information to complete their individual Form 1040. W-2 Salary, Distributions, and Form 1040 (The Owner’s Perspective) If you own and work for an S corp, you must

Am I the Only One Bad with Money? The Psychology Behind Financial Procrastination

Ever feel like your finances are a mess, and you’re just “bad with money”? You’re not alone, and it’s probably not entirely your fault. Many Americans struggle with financial organization. A survey by Ally Financial found that 45% of us are concerned about our finances, and 46% let emotions influence our spending. Yet, despite this emotional connection to spending, 36% never seek support for managing their money. This highlights a key point: there’s a lot of psychology behind why we struggle. Let’s explore these hidden factors and how you can take control! Table of Contents How Organized Are Your Finances? Take This Quiz to Find Out Ready to see how financially organized you really are? Take a quick look at the list below and check off any of these situations that apply to you. It’s a good way to get a clearer picture of where you stand. Don’t worry, you’re not alone if you checked some of these. But if you marked more than five, it’s time to take a closer look at what’s going on. While it’s common to focus on your work or business, neglecting your finances can create serious problems down the road. Let’s explore the psychological factors that contribute to financial disorganization and learn how to master your money. Bad Financial Organization: What and Why? So what is bad financial organization? It’s more than just feeling “bad with money”—it’s a bunch of habits that slowly eat away at your financial well-being. Consider missed payments, clueless spending, no emergency fund, stress shopping, and that constant worry about debt. These are all signs you’re not in control of your money. Why does this matter? On a personal level, it can lead to a ton of stress, anxiety, and even fights with your partner. But financial messes can have way bigger consequences. Remember Enron? They were huge. But they were also faking it ’til they made it (or, well, didn’t make it). They used all sorts of accounting tricks to hide their debt and make their profits look way better than they actually were. When it all came crashing down, it was a mess – lost jobs, ruined reputations, the whole nine yards. It’s an extreme example, but it shows that messing with finances, whether it’s billions of dollars or your weekly grocery budget, can seriously backfire. And here’s the thing: it’s not always about knowing the right formulas. Sure, understanding finances is important, but there’s often more going on. Things like fear, avoidance (who wants to look at those bills?), impulsive spending, and even money habits you picked up from your family can play a big role. These hidden influences can totally wreck your best intentions. So, if you’re struggling, it’s not just about learning how to balance a checkbook, It’s about figuring out why you do the things you do with your money. Let’s explore the psychology of bad financial organization and see what’s really happening. The Psychological Roots of Bad Financial Habits Here are some common psychological factors that influence our finances: Breaking the Cycle: Taking Control So, you’ve discovered that your brain isn’t always rational when it comes to money. Acknowledging the problem is the first step. Now, think of yourself as a machine. Even with the same “input” (financial challenges), changing your operating system (financial habits) can lead to a much brighter financial future. It’s like upgrading your software – you can handle the same stuff, but way more efficiently. Here’s your user manual for the upgrade: Next time you feel like you’re “bad with money,” remember the psychology behind it. You’re not alone, and you can take control. Ready to get started? Schedule a call with us – we can help you develop a plan and conquer those financial challenges.

Freelancing in 2025: Your Guide to Thriving in the Gig Economy

The pandemic flipped the traditional 9-to-5 workday on its head, and freelancing is here to stay. More and more people are ditching the office for the flexibility and freedom of working from home. This article dives into the freelancing trend, explores the ups and downs, and gives you actionable tips to succeed. Want to know if freelancing is right for you? In this article, we’ll explore the state of freelancing in the U.S., analyze the benefits and challenges, and share practical tips to help you make informed decisions. Table of Contents The US Freelance Scene: A Quick Look Service Offered Hourly Rate Range Equivalent Annual Salary Web Development $50-60 $69,000 Mobile Development $55-65 $75,000 Graphic Design $40-45 $53,000 Content Editor $25-35 $38,000 Copywriter $30-40 $44,000 Programmer $60-70 $81,000 Online Marketing/SEO $40-50 $56,000 CRM Management $50-60 $69,000 Data Analysis $55-65 $75,000 The Freelance Challenge Freelancing offers incredible freedom, but it’s not always sunshine and rainbows. Here are some of the hurdles you’ll likely encounter: The Freelance Opportunity Despite the challenges, freelancing offers incredible potential. Here are some of the exciting opportunities available: Tips for Freelance Success Useful Resources for Freelancers Ready to jump into freelancing and keep your finances organized? Schedule a call with our experts to simplify your accounting!

Fynlo & VA Bar: Empowering the Team Behind 18,000 Dreams

VA Bar isn’t just an academy—it’s a launchpad. A launchpad for 18,000 dreamers, each chasing their own version of freedom. Some want to escape the 9-to-5 grind, others dream of building a career that fits around family life, and many simply want to take control of their financial future. VA Bar gives them the wings—training in essential digital skills like social media, design, lead generation, and SEO. But even the strongest wings need fuel. And for freelancers, that fuel is financial clarity. Table of Contents Where Fynlo Comes In We’re not just building accounting software; we’re bridging the gap between ambition and achievement. We know the struggle—the late nights staring at spreadsheets, the frustration of financial jargon, the constant worry about getting it “right.” Our mission is simple: to make finances effortless, to give freelancers the confidence to grow, and to free them from the admin that holds them back. From Two Days of Drudgery to Days of Impact At VA Bar, the staff and tutors pour their energy into nurturing 18,000 dreams. But before Fynlo, two full days each month were lost to invoicing, payments, and record-keeping—precious time that could have been spent mentoring students, developing courses, and strengthening the VA Bar community. Not anymore. “We’re here to change lives, not chase invoices. Fynlo gives us the freedom to focus on what really matters—empowering our students to succeed.” — Ms. Tetchie, VP of Operations at VA Bar At VA Bar Academy, we are dedicated to empowering individuals through comprehensive upskilling and real-life experiences. Our mission is to provide top-quality virtual assistance training, equipping students with the skills and confidence needed to excel in virtual work environments. We emphasize practical learning by offering internships that immerse our students in real-world scenarios, fostering both personal and professional growth. Additionally, we prioritize economic advancement by providing job placement opportunities, ensuring a clear path to success for our graduates. We are committed to creating an inclusive and supportive community where everyone can learn, grow, and thrive. Continuous improvement and innovation drive us to enhance our programs, preparing our students to meet the evolving demands of the virtual workspace. — Girlie E. Feratero, CEO/Founder at VA Bar A Partnership Driven by Passion Right now, a small team at VA Bar is using Fynlo—but that’s about to change. Soon, the entire team will have access to the same powerful tool that’s already making their lives easier. More time. More focus. More impact. This partnership isn’t just a business decision; it’s a shared mission. VA Bar and Fynlo share the same values—empowerment, innovation, and an unwavering commitment to customer success. We’re not just collaborating; we’re fuelling a movement. More Than Numbers — A Brighter Future We’re not just managing finances; we’re enabling possibilities. We’re not just streamlining processes; we’re giving educators the time and confidence to mentor the next generation of virtual assistants. Those two days a month? They’re no longer lost to admin. Now, they’re filled with creativity, student support, and real impact. Join us in transforming financial management for everyone. Whether you’re an entrepreneur, a freelancer, an educator, or simply someone looking to gain better control of your finances, Fynlo and VA Bar are here to support you. Try Fynlo today and experience the confidence that comes with financial clarity.

10 Absurdly Clever Tax Deductions That Got Approved

The IRS has seen some pretty wild tax deduction attempts over the years, and some of them actually worked! Check out our list of the 10 craziest tax deductions you have ever heard of! And if you’re a freelancer, don’t miss our other blog: “The Freelancer’s Guide to Tax Deductions.” Table of Contents 10 Wild Tax Deductions Legit Deduction or Wishful Thinking? Let’s Find Out! Now that you’ve seen some of the most surprising tax deductions that actually got approved, it’s time to test your own deduction savvy. Below are a few expenses. For each, one scenario is deductible, and the other isn’t. Can you determine which is which?Cat FoodScenario 1: Junkyard owner buys food for rat-patrolling felinesScenario 2: Snack for a pet catGuard DogScenario 1: Business guard dog expensesScenario 2: Pet dog expensesTutorsScenario 1: Specialized tutor for a child with a diagnosed learning disability, as recommended by their doctorScenario 2: Reading tutor for general academic improvementAfrican SafariScenario 1: Dairy business owners on a wild animal-focused tripScenario 2: Family vacationPrivate AirplaneScenario 1: Condo owners flying themselves to check on their rental propertyScenario 2: Vegas private jet ride Personal TrainerScenario 1: Trainer for a professional athleteScenario 2: Gym-goer getting ready for summerClown CostumesScenario 1: Professional clown costumeScenario 2: Halloween costumeSun ProtectionScenario 1: Sunscreen for carpenters/gardenersScenario 2: Sunscreen for beach trip Absolutely right! Scenario 1 is deductible, but Scenario 2 isn’t. Many of these cases are based on real stories, proving that the same expense can be approved or denied depending on the context and whether it meets the IRS rule of ‘ordinary and necessary.’ “Ordinary” means it’s common in your line of work, and “necessary” means it’s helpful and appropriate for your business—not just something you want. Tax deductions come with rules. For example, guard dog expenses are only deductible for the time the dog is actually working, and medical deductions are subject to limitations like the 7.5% AGI rule. Because tax laws are complex, it’s always best to consult a professional when in doubt. Itemized Deduction vs. Standard Deduction These unusual (and sometimes surprisingly successful) deductions highlight the importance of understanding the rules and keeping meticulous records. Navigating the tax code can be tricky, and knowing what qualifies as a legitimate deduction is crucial for any taxpayer. This is especially crucial when deciding whether to itemize or take the standard deduction. The TCJA changed the tax landscape, making the standard deduction the better option for most taxpayers. But if you have significant deductible expenses, itemizing can still work in your favor. The good news? The old deduction limit is gone, so you can claim the full amount if eligible. That said, with fewer people itemizing, the IRS is paying closer attention to those who do. If you’re planning to itemize, make sure your records are solid. Looking to keep your records organized and ready for tax filing? Schedule a call with our experts today for bookkeeping support.