Picking the right business structure is a big deal, and taxes are a huge part of that decision. In this article, we’re breaking down the tax filing side of things for C Corps, S Corps, and LLCs, so freelancers and business owners can get a handle on the forms and deadlines for each. If you’re looking for a broader comparison, Choosing the Best Business Structure for Freelancers is a solid starting point!

The article was last updated as of 4 March 2025. Keep in mind that tax rules and limits can change, so be sure to watch out for updates or consult a tax professional for the latest information.

Table of Contents

- Brief Highlights: Comparing C Corp, S Corp and LLC

- S Corporation Tax Filing

- C Corporation Tax Filing

- LLC Tax Filing

Brief Highlights: Comparing C Corp, S Corp and LLC

Here’s a quick rundown of the three business structures to give you the big picture. In the next sections, we’ll break down the details of tax treatment and the specific forms you’ll need to know. It’ll all come together as we go.

| Category | S Corporation (S Corp) | C Corporation (C Corp) | Limited Liability Company (LLC) |

| Tax Forms | – Form 1120-S – Shareholders file Schedule K-1 on personal returns | – Form 1120 – Shareholders report dividends on personal returns | Depends on tax classification. See LLC section. |

| Filing Deadlines | March 15 2025*; extensions available | April 15 2025*; extensions available | Depends on tax classification. See LLC section. |

| State Taxes | Varies; some states do not recognize S Corp status | Subject to state corporate income taxes | Subject to state taxes depending on classification |

| Eligibility Requirements | – Must be a domestic business – Up to 100 shareholders – Individuals only | – No limit on shareholders – Can include foreign and corporate owners | – No ownership restrictions – Flexible member structure |

| Ownership Restrictions | – Max 100 shareholders – One class of stock – U.S. citizens/residents only | – Unlimited shareholders – Can issue multiple stock classes | – No restrictions – Members can be individuals, corporations, or foreign entities |

| Compliance Requirements | – Annual meetings – Shareholder voting – File annual reports | – Annual meetings – Corporate governance – Strict record-keeping | – Varies by state – Fewer formalities than corporations |

| Average Formation Costs# | ~$1,200 | ~$633 | ~$50-$500 depending on state |

| Fundraising Ability | – Limited – Cannot issue preferred stock | – High – Can issue both common and preferred stock | Limited unless electing C Corp tax treatment |

| Dividend Taxation | Distributions taxed once at shareholder level | Dividends taxed twice (corporate and shareholder level) | Not applicable unless taxed as C Corp |

| Payroll Tax Implications | Must pay reasonable salary to shareholder-employees | Corporate officers are employees subject to payroll taxes | Members typically pay self-employment tax unless S Corp election made |

| Passive Income Limits (such as rent, interest, or certain royalties) | Passive income limited to 25% of gross receipts | No passive income limitations | No passive income restrictions |

| Liability Protection | Protects shareholders’ personal assets | Protects shareholders’ personal assets | Protects members’ personal assets |

| Conversion Flexibility | Can convert to C Corp; changing to LLC requires dissolution | Can convert to S Corp or LLC with filings and approvals | Can elect S Corp/C Corp taxation; conversions depend on state rules |

| Foreign Ownership | Not allowed | Allowed | Allowed |

| Administrative Burden | Higher than LLC; less than C Corp | High due to strict governance requirements | Low; fewer formalities required |

| Key Tax Advantages | – Avoids double taxation – QBI deduction available | – Potential for certain deductions not available to pass-through entities – Can deduct health insurance premiums for employees | – Flexible tax treatment (can choose to be taxed as a partnership, S corp, or C corp) – Simpler tax compliance than C-corp if taxed as a partnership |

| Key Tax Disadvantages | – Reasonable salary requirement – Limitations on QBI deduction for certain businesses | – Double taxation – More complex tax compliance | – Members subject to self-employment tax (unless taxed as C-corp) – Less established than C-corps in some states |

| Best For | Small businesses seeking tax savings through pass-through taxation | Larger businesses seeking growth through investment and stock issuance | Startups, freelancers, or small businesses needing flexibility |

* For calendar-year corporations, Form 1120 is due on April 15, and Form 1120-S is due on March 15. For fiscal-year corporations, the deadline is the 15th day of the fourth month (1120) or third month (1120-S) after the fiscal year ends.

# Formation costs vary by state and the scope of professional services.

S Corporations Tax Filing

S corps offer a unique tax structure, blending the legal benefits of a corporation with the tax advantages of a partnership. This pass-through taxation model avoids the double taxation burden of C corporations, making it an attractive option for many small businesses.

Pass-Through Taxation

One of the most significant advantages of an S corporation is its pass-through taxation model. Unlike C corporations, which are subject to double taxation (taxed at both the corporate and shareholder levels), S corps do not pay federal income tax at the corporate level. Instead, the corporation’s profits and losses are passed through to the shareholders, who report them on their individual tax returns (Form 1040). This structure avoids the double taxation burden and can result in significant tax savings for business owners.

Form 1120-S

Form 1120-S, the U.S. Income Tax Return for an S Corporation, is the primary form S corps use to report income, deductions, gains, and losses to the IRS. It ensures the corporation’s financial activity is accurately reported and provides shareholders with the information needed to complete their individual tax returns.

The form is due by March 15th for calendar-year taxpayers (or the 15th day of the third month after the fiscal year ends). If additional time is needed to prepare the return, S corps can request an extension using Form 7004, which grants an automatic six-month extension. However, it’s important to note that an extension to file does not extend the deadline for paying any taxes owed. Estimated tax payments must still be made by the original due date to avoid penalties and interest.

Schedule K-1

Schedule K-1 details each shareholder’s individual share of the corporation’s income, deductions, credits, and other tax items. Shareholders use this information to complete their individual Form 1040.

W-2 Salary, Distributions, and Form 1040 (The Owner’s Perspective)

If you own and work for an S corp, you must pay yourself a “reasonable salary” for the work you do. This salary is subject to income tax, Social Security, and Medicare, and it’s reported on your personal tax return (Form 1040). On top of your salary, you may also receive distributions, which are your share of the S corp’s profits. These distributions, along with any business losses, are reported on Schedule E of your Form 1040. The key benefit here is that only your salary is subject to payroll taxes, while distributions are not, which can help lower your overall tax burden.

Finding the right balance between salary and distributions is essential. Paying too little salary can raise red flags with the IRS, as it may look like you’re trying to avoid self-employment taxes. On the other hand, paying too much salary means missing out on potential tax savings. The IRS requires “reasonable compensation,” which is typically determined by comparing your role, skills, and experience to what someone else would earn for similar work in your industry. By properly balancing your salary and distributions, you stay compliant with IRS rules while maximizing your tax efficiency.

Tax Rates & QBI Deduction

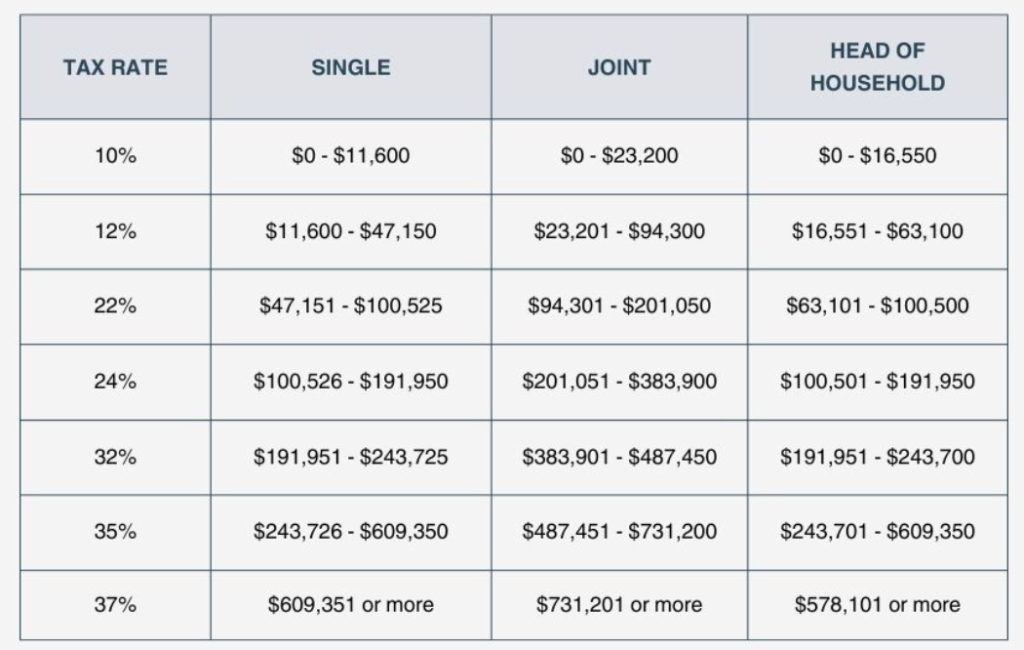

The tax rate an owner or shareholder pays on S corp profits is based on their individual income tax rate, which ranges from 10% to 37%, depending on their total taxable income. This means the amount of tax owed on S corp income varies based on the shareholder’s overall financial situation.

2024 Tax Rates for a Single Taxpayer (Source)

Additionally, shareholders may qualify for the Qualified Business Income (QBI) deduction, a tax break introduced in 2018 that allows them to deduct up to 20% of their share of the S corp’s income. This deduction can significantly lower taxable income, making the S corp structure even more attractive for small business owners.

The QBI deduction applies to self-employed individuals and small business owners, including S corp shareholders. According to the IRS, QBI is defined as “the net amount of qualified items of income, gain, deduction, and loss from any qualified trade or business.” For most U.S.-based businesses, this typically means QBI equals the business’s net profits. By reducing taxable income, the QBI deduction not only lowers tax liability but also supports growth and investment in small businesses, making it a valuable benefit for S corp owners.

State and Local Taxes

While federal regulations are paramount, S corps must also comply with state and local tax laws, which vary significantly. Some states recognize the federal S corp election and follow pass-through taxation, while others may treat S corps differently or impose additional filing or tax requirements. In some cases, states even have their own S corp election process. If your S corp operates in multiple states, the complexity increases, as each state may have unique rules. Consulting a tax professional is crucial to navigate these variations and ensure compliance with all state and local tax obligations.

Estimated Taxes

Since S corp profits are passed through to shareholders, they are not subject to withholding like a regular paycheck. As a result, shareholders often need to make estimated tax payments throughout the year. If a shareholder’s tax liability related to their S corp income exceeds $1,000, they are generally required to make these payments to avoid penalties. Accurate calculation and timely payment of estimated taxes are critical for S corp owners to stay compliant and avoid unnecessary fines. Proper planning and working with a tax professional can help ensure these payments are managed effectively.

C Corporations Tax Filing

C corps are a popular business structure, but their tax rules can be tricky. For C corp owners, understanding the basics, like tax forms, double taxation, and deductions, is key to keeping the business running smoothly and taxes under control. If more time is needed to file, you can request a six-month extension by submitting Form 7004.

Double Taxation

C corps face something called double taxation. This means the company’s profits are taxed twice:

- First, at the corporate level when the business earns money.

- Then, at the shareholder level when profits are paid out as dividends.

For example, if a C corp makes 100,000 in profit, it pays a 21,000 in taxes. The remaining 79,000 can be given to shareholders as dividends. If a shareholder gets 10,000 in dividends, they must pay taxes on that amount at their personal tax rate. This double layer of taxes is a major difference between C corps and other business types like S corps or LLCs.

Form 1120

C corporations use Form 1120 (U.S. Corporation Income Tax Return) to report their income, expenses, and taxes to the IRS. Think of it as the business equivalent of an individual’s Form 1040.

For calendar-year corporations, Form 1120 is due by April 15. For fiscal-year corporations, the deadline is the 15th day of the fourth month after the fiscal year ends. If needed, corporations can request a six-month extension by filing Form 7004, pushing the deadline to October 15 for calendar-year corporations.

Form 1120 covers everything from total revenue and operating expenses to deductions and tax credits, ultimately determining the corporation’s tax liability.

Estimated Taxes

C corps must pay taxes quarterly, meaning four times a year. They estimate how much tax they’ll owe for the year and make payments using the Electronic Federal Tax Payment System (EFTPS). If they don’t pay enough or miss deadlines, they could face penalties. To avoid extra costs, make sure to stay on top of these payments and meet all deadlines.

Deductions and Expenses

C corporations can deduct many common business expenses. These include things like salaries and wages, rent, depreciation, interest expense, advertising expenses, repairs and maintenance and interest on loans. However, not all expenses are deductible, and some deductions have limits. Check out “The Freelancer’s Guide to Tax Deductions: Keep More of Your Cash” to find out more about what is deductible. And for a bit of tax-related amusement, you won’t believe these 10 Absurdly Clever Tax Deductions That Got Approved. Given the complexity of tax law, consulting with a tax professional is essential to ensure your C corp is taking advantage of all available deductions.

State and Local Taxes

On top of federal taxes, C corps may also owe state and local taxes. These vary widely—some states charge corporate income taxes, while others have franchise taxes or other fees. If the business operates in multiple states, the rules can get even more complex. Consulting a tax professional is highly recommended to ensure compliance and avoid surprises.

LLC Tax Filing

LLCs (Limited Liability Companies) are unique because they combine the liability protection of a corporation with the tax flexibility of a sole proprietorship or partnership. How an LLC is taxed depends on its structure and the choices made by its owners. Here’s a breakdown of how LLC tax filing works, including the different tax classifications and what each one means for your business.

Flexible Tax Options

LLCs are created at the state level, but the IRS treats them differently depending on their ownership structure and tax election. By default:

- A single-member LLC (one owner) is taxed as a sole proprietorship.

- A multi-member LLC (multiple owners) is taxed as a partnership.

Both sole proprietorships and partnerships are pass-through entities, meaning the business itself doesn’t pay taxes. Instead, profits and losses “pass through” to the owners, who report them on their personal tax returns. This avoids double taxation, a key benefit of the LLC structure.

However, LLCs aren’t limited to these default classifications. They can also choose to be taxed as an S corporation or C corporation if it benefits their tax situation. This flexibility allows LLC owners to pick the tax treatment that works best for their business.

Tax Classifications

How an LLC is taxed depends on the tax classification it chooses. LLCs are unique because they offer flexibility in how they are taxed, allowing owners to select the option that best suits their business needs. Below is a summary of the four main tax classifications for LLCs, followed by a detailed explanation of each:

| Tax Classification | Description | Key Forms | Filling Deadlines for Calendar-Year Businesses | Tax Implications |

| Single-Member LLC | Treated as a sole proprietorship by default. | – Schedule C (Form 1040) – Schedule SE | 15 April 2025 | Income taxed at owner’s individual tax rate (10%-37%). Self-employment taxes apply. |

| Multi-Member LLC | Treated as a partnership by default. | – Form 1065 – Schedule K-1 – Schedule E – Schedule SE | 15 March 2025 | Income passes through to members, taxed at individual rates. Self-employment taxes apply. |

| LLC Taxed as C Corporation | Elects C corp status by filing Form 8832. | – Form 1120 | 15 April 2025 | Subject to 21% corporate tax rate. Dividends taxed again at individual level (double taxation). |

| LLC Taxed as S Corporation | Elects S corp status by filing Form 2553. | – Form 1120-S – Schedule K-1 | 17 March 2025 | Income passes through to owners, taxed at individual rates. Self-employment taxes apply only to salary. |

Now, let’s explore each classification in more detail.

1. Filing Taxes as a Single-member LLC

For single-member LLCs that haven’t elected corporate taxation, federal income taxes are filed as a sole proprietorship. This involves reporting business income and expenses on your personal Form 1040, with taxes calculated at your individual income tax rate. Specifically, you’ll use Schedule C to calculate and report your LLC’s profits or losses, requiring an income statement and detailed financial records for deductions. Additionally, self-employment taxes (Social Security and Medicare) are reported and paid via Schedule SE.

2. Filing Taxes as a Multi-member LLC

Multi-member LLCs, in their default state, file as partnerships unless they elect corporate taxation. Specifically, the LLC uses Form 1065 to report its income and losses to the IRS. Also, the LLC prepares Schedule K-1 for each member, detailing their share of the business’s profits, losses, deductions, and credits. Subsequently, members use their K-1 to report these items on their individual Form 1040. To get Form 1065 done right, you’ll need year-end financial statements, like a profit and loss statement, a list of deductible expenses, and balance sheets for the beginning and end of the year. Finally, members report their share of business profits or losses on Schedule E and calculate self-employment taxes using Schedule SE.

3. Filing Taxes as a S Corporation

LLCs can choose to be taxed as S corporations by filing Form 2553 with the IRS. This election allows the LLC to pass its income, credits, and deductions through to its members, similar to a partnership or sole proprietorship. The primary advantage of this election is related to self-employment tax; while sole proprietorships and partnerships pay self-employment tax on a100% of the profits, S corp owners only pay it on their salary. LLCs taxed as S corporations file Form 1120-S, and members receive Schedule K-1s to report their share of income or losses on their personal tax returns.

4. Filing Taxes as a C Corporation

If an LLC’s members decide that C corporation tax status would reduce their overall tax burden, they can file Form 8832 with the IRS to make that election. This changes the LLC’s tax treatment; the IRS then views the LLC as a separate taxable entity. So, the LLC now files its own separate tax return, Form 1120, to report its income, deductions, and other financial details. This separates the LLC’s tax liability from the owners’ personal tax obligations. Similar to preparing Schedule C, you’ll need comprehensive financial records to complete Form 1120.

Which choice is right for you depends on multiple factors. Choosing to file as a corporation, for example, can save you money on self-employment taxes but requires stricter reporting. When determining what your LLC should file as, discussing your options with a CPA or tax professional ensures you’re making the best choice.

Tax Rates

The tax rates for LLCs vary based on the tax classification they select. Since LLCs don’t have a set tax rate, they follow the tax rates of the entity type they choose. Here’s how it works:

Single-member LLCs (Sole Proprietorship): Income from a single-member LLC is taxed at the owner’s personal income tax rate, which ranges from 10% to 37% federally, depending on their total taxable income.

Multi-member LLCs (Partnerships): Similar to single-member LLCs, multi-member LLCs are taxed at the individual tax rates of each member. Each owner reports their share of the LLC’s profits or losses on their personal tax return, based on their individual tax bracket.

LLCs taxed as C Corporations: LLCs electing C corporation status are subject to a flat federal corporate tax rate of 21% on their net income. However, if profits are distributed to members as dividends, those dividends are also taxed at the individual level, resulting in double taxation.

LLCs taxed as S Corporations: S corporations do not pay corporate income tax. Instead, income passes through to the owners, who are taxed at their individual tax rates. Owners must pay self-employment taxes (Social Security and Medicare) on their salary, but distributions are not subject to these taxes, offering potential tax savings.

With a solid grasp of the tax filing differences between C Corps, S Corps, and LLCs, you’re well on your way to making informed decisions for your business. Need personalized tax advice? For personalized tax advice, schedule a call with us.